In The Week

You’re on the free list for Formal Verification research. Join the other Formal Verification members today and receive complete research and member-only bonus content.

Spotlight 🔎

Augur

Augur V2 has launched on mainnet.

Augur’s V2 brings a suite of improvements to offer a more refined experience for end users, including USD denominated markets through MakerDAO’s DAI, Uniswap’s V2 oracle system for price feeds, as well as 0x’s off-chain order books. Augur’s trading UI is the only one of the 3 open-source UIs that is currently live. Current REP holders are required to manually migrate their REP to the new V2 token in order to participate in Augur’s new reporting system.

The Formally Verified Take

Although only a few days since launching, Augur V2 has encountered a wide set of issues that have made initial usage near impossible. With current Ethereum congestions, users have reported paying ~$30 to create an account and upwards of $40 to withdraw their funds (e.g. DAI) from Augur contracts due to the gas required to execute the contract logic.

Additionally, there have been Augur-specific bug issues, particularly on the front-end, which has hindered any meaningful adoption so far. For example, account activations have often failed requiring users to deposit amounts within a certain bound (40-100 DAI). On top of this, users have reported seeing overestimated gas costs requiring users to rely on other 3rd parties like Metamask. This has lead developers to quickly work on several long-term solutions just when the community thought the V2 roadblocks had ended.

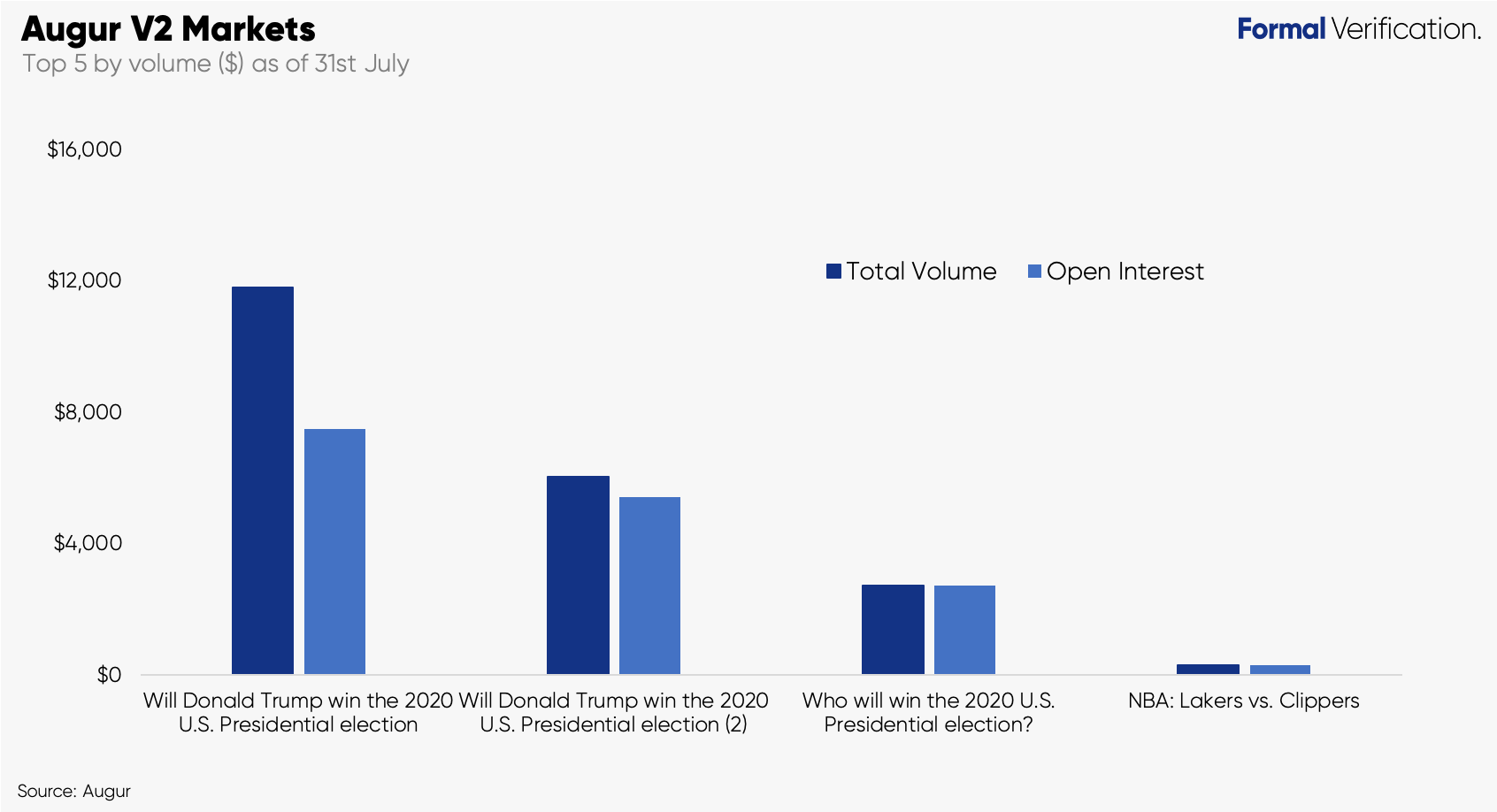

Looking at the numbers, there are only 4 markets with any volume or open interest, most of which centre around the 2020 U.S. Presidential election - the largest market having just under $12k in volume.

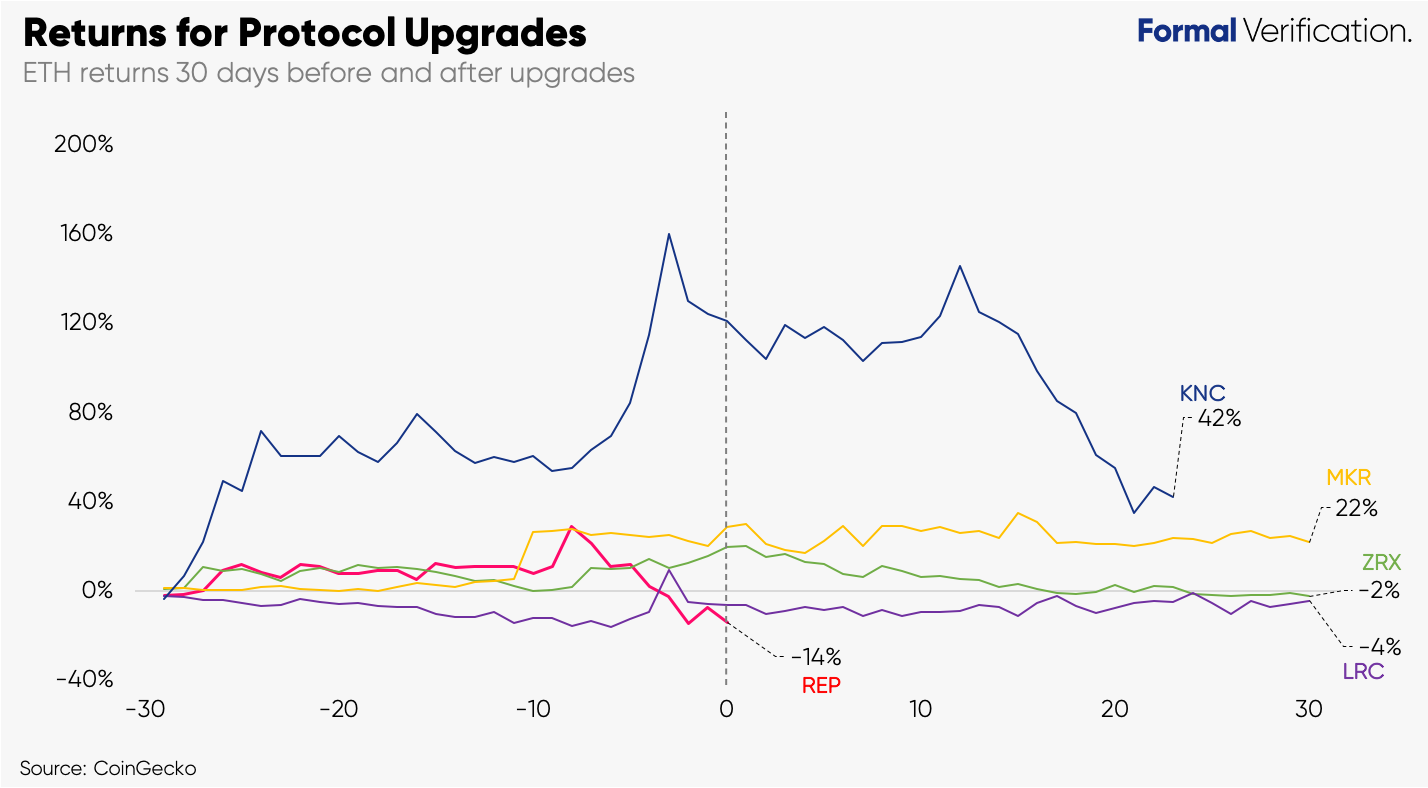

These UI problems are important to consider because they directly impact any meaningful volume/open interest on the protocol, therefore impacting Augur reporter fees and REP valuation. The lack of market interest in Augur V2 combined with stronger ETH price action has lead to negative REP performance against ETH in the last month. Comparing this to other protocol launched, most cryptoassets experience price appreciation in the lead up to their respective upgrades over the same time period of 30 days.

Note that protocol upgrade can take place in entirely different market sentiments making a direct comparison difficult. However, it can still nonetheless provide an insight into market sentiment around protocol upgrades.

While it is still incredibly early, Augur will have to quickly fix current issues and find its niche in a growing competitive prediction markets and options landscape: FTX already allows for users to take part in election betting. Synthetix has now introduced binary options. Opyn recently launched with ETH protective call and put options. Omen and Polymarket have also entered the scene using Gnosis’ conditional token framework enabling interdependent events and higher resolution forecasting.

As always, Augur’s success will rely on effective incentivisation within its niche that will encourage network and market participation, driving significant network proliferation in the process.

Quick Takes ⚡️

Aave

Aave introduces token upgrade proposal - Aavenomics.

A plethora of protocol-level changes have been proposed that aim to decentralise the network to key stakeholders (i.e. Aave token holders). In short, Aave holders will be able to vote on key policies that define the rules of the protocol. Like many other networks, Aave Improvement Proposals (AIPs) can be created and requested by holders. LEND, Aave’s original token, will migrate to AAVE via a Genesis Governance vote, at a rate of 100:1.

The Formally Verified Take

An incentive design overhaul and move towards greater decentralisation echoes very much what we’ve seen with other DeFi protocols - Compound, Kyber, and Curve to name just a few. Aave will now distribute incentives for those participating in the network directly. In other words, users supplying and borrowing assets.

What’s particularly interesting about Aave’s new proposition is the composable design of the safety module. As well as receiving AAVE directly, AAVE stakers can also earn rewards by supplying to the AAVE/ETH pool on Balancer. While this establishes further reward streams for securing the Aave protocol overall, this also means that Aave’s incentive structure is partially dependent on the security of Balancer.

As it currently operates, LEND is periodically burned from collected fees accrued by the protocol. One of the important decisions that the community will have to decide on is whether burning also extends to AAVE or if any collected fees can flow directly to stakers themselves. Over time, it is reasonable to expect that the community would prefer direct value flow distribution - this sentiment around cryptocapital assets continues to grow in other parts of the ecosystem (see Kyber’s latest reward fee distribution in the KyberDAO).

Pods

Help Build Decentralised Networks 🌍

Formally verified Web 3.0 roles are available for full Formal Verification members.

Formal Verification Deal Sheet 🤝

Formal Verification is proud to have partnered with some of the leading crypto companies. The deal sheet is now available to see for full Formal Verification members here.