In The Network - DEX Aggregators

Adoption, Evolution, Efficiencies

This Formal Verification research is free for everyone. Join the other Formal Verification members today and get full access to complete research and member-only bonus content.

DEX Aggregators

With the number of decentralised exchange (DEX) venues in DeFi climbing by the week, the value proposition of DEX aggregators increases too. DEX aggregators (1inch, 0x API, DEX.AG, Paraswap, Totle) pull fragmented liquidity from a number of exchanges to offer limited slippage, best exchange prices, and clean UIs. They ultimately serve their end users.

DEX aggregators seen today provide rich sets of features, deeper liquidity, and more effective measures to abstract away smart contract complexity. This has translated into phenomenal growth in exchange volume this year for certain aggregators. One of these aggregators is 0x’s API, which launched in late January which helps developers and applications gain access to liquidity from numerous sources including 0x Mesh, Uniswap, and Kyber. In July alone, 0x API facilitated $120 million in volume.

However, the dominant DEX aggregator in the market is 1inch - a total of $1.3 billion has been traded through the aggregator so far this year. 1inch is similar to the 0x API in its overall aim of bridging multiple DEX venues but uses a combination of centralised off-chain order book swaps and on-chain swaps that is facilitated by OneSplit.

One of the strengths of 1inch as a DEX aggregator is that it supports a wide range of live integrations which have played a key role in allowing users to capitalise on yield farming opportunities. Yet, 1inch has become an increasingly prominent player within DeFi more generally. Today, 1inch launched its own automated market maker (AMM) called Mooniswap, which enables liquidity providers to receive a portion of price slippage profits. Mooniswap as a liquidity source has already been integrated and 1inch can already start leveraging Mooniswap in its fight to become a horizontal monopoly.

While 0x API and 1inch have shown some success, other aggregators, such as DEX.AG, Totle, and Paraswap have all failed to capture any significant long-term market share throughout this year.

We might be curious to know how much DEX trading activity is facilitated by aggregators. As we can see below, comparing the total volume facilitated by aggregators to total DEX volume shows that aggregators have taken up an increasing share of total DEX volumes this year. At its peak in June, aggregators made up 45% of total DEX volume but has since subsided to ~8%.

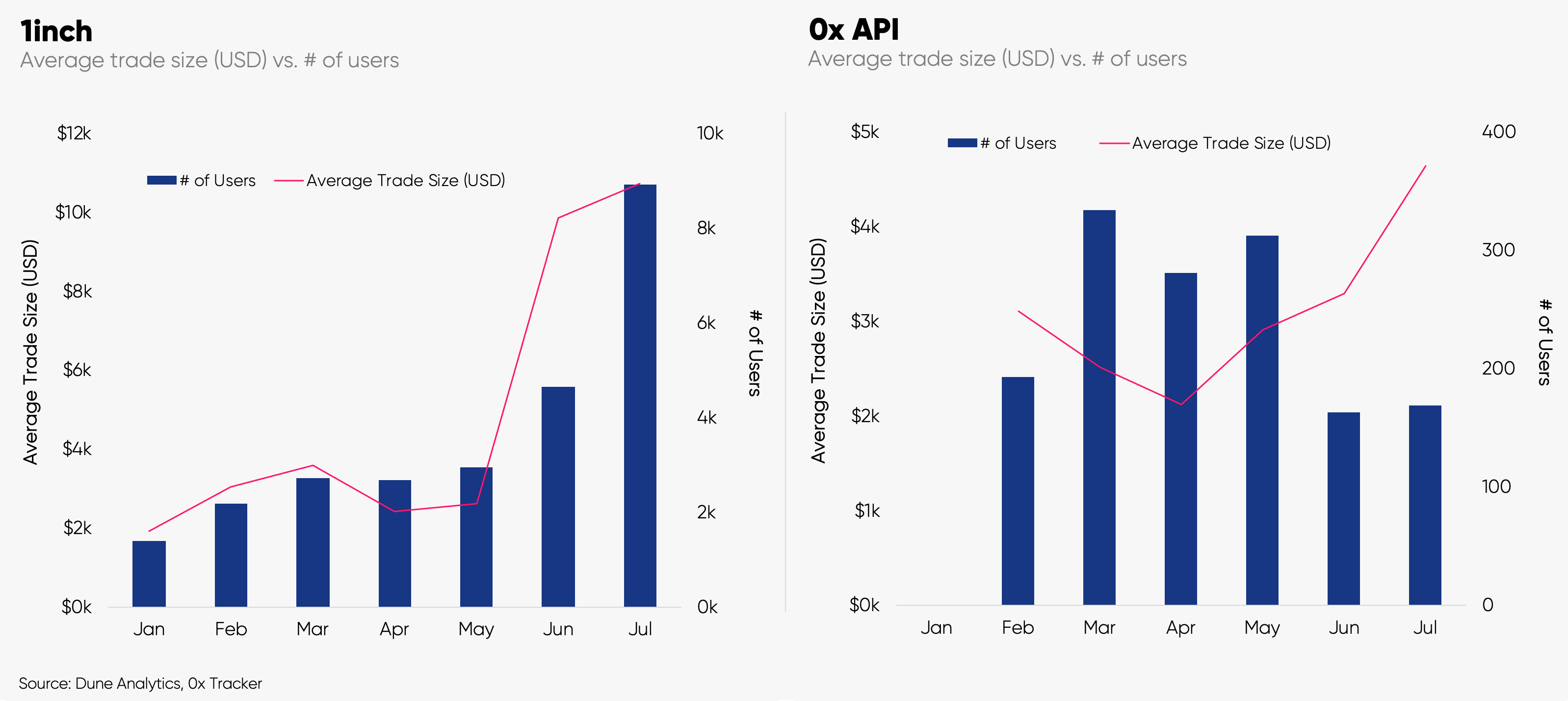

Average trade size is an important metric for any aggregator or exchange. Comparing the two market leaders, both 1inch and 0x API have seen an increase in average trade size over the last 4 months. However, 1inch users are trading on average ~$5.5k more than users trading with 0x API. There are also differences with user trends. 1inch has also had month-on-month growth in the number of unique users trading with the aggregator since January whereas user count for the 0x API peaked in March at 330.

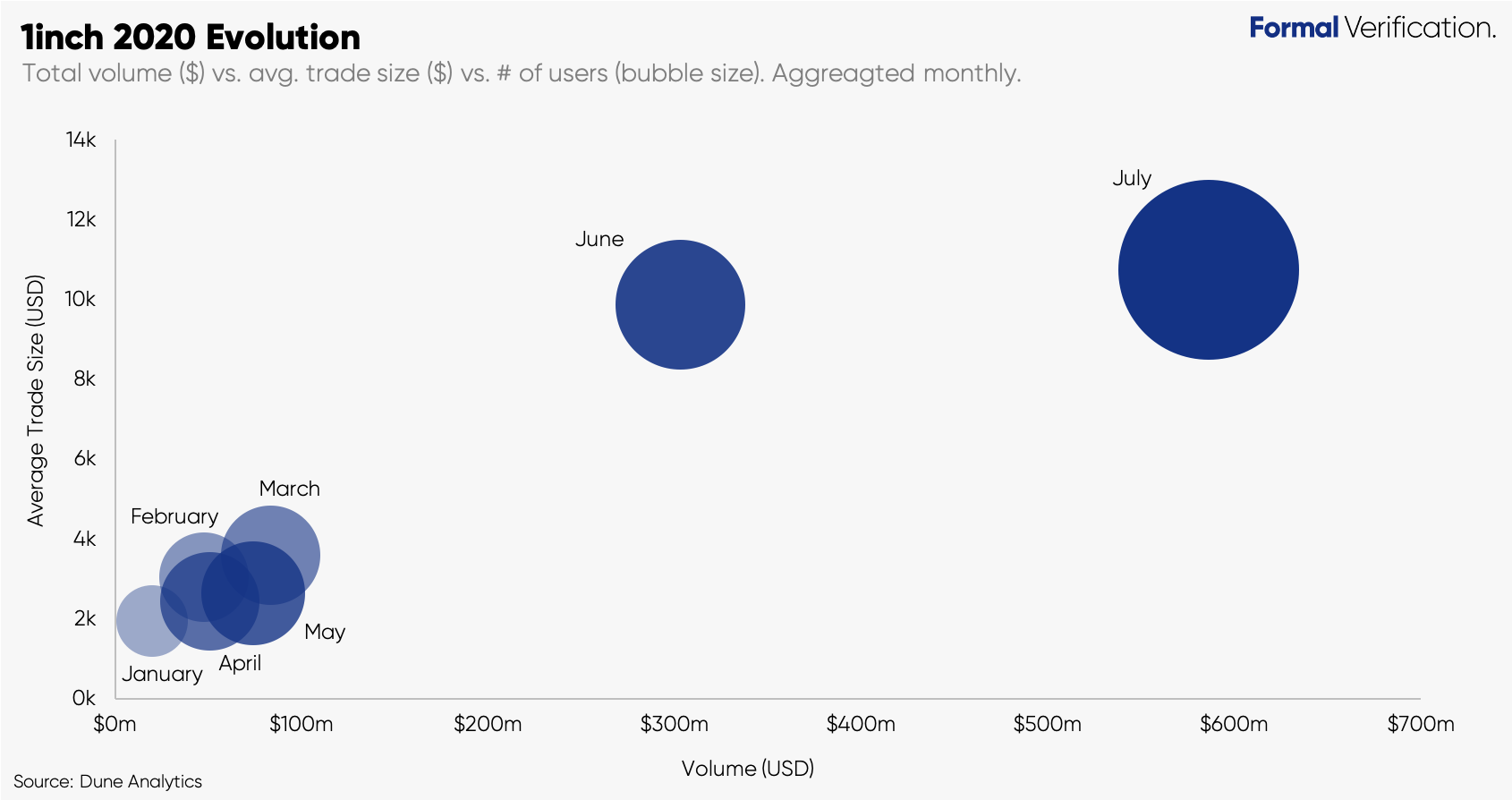

Combining the data from the three metrics above (trading volume, avg. trade size, user count) for 0x API and 1inch in a single bubble graph can provide a richer insight into how each aggregator has evolved over time. Just like we touched on earlier, 0x API has shown impressive growth in volume in July but still lacks a clear pattern in any of the three metrics

On the other hand, 1inch exhibits a much clearer pattern of growth each month shown by the movement of bubbles to the top right corner as well as the growing size of the bubbles themselves over time. This may indicate that 1inch has achieved product-market fit.

One of the problems of order splitting that 1inch has actively tried to mitigate is the high cost associated with numerous smart contract interactions. 1inch does this by integrating GasToken directly into its own smart contracts which allows users to store gas by minting Gastokens when prices are cheap and burn them during periods of high gas prices.

As highlighted in previous issues, integrating GasToken has meant that users have still been able to experience efficient swaps while keeping overall transaction fees down. Up until June, users were able to use the older Gastoken standard (GST2) for their orders before the 1inch developers introduced an improved token standard called CHI. In short, CHI improved efficiencies regarding the smart contract address size and burning process. The result being that CHI is 1% more efficient for minting and 10% more efficient for burning (CHI optimisation represented by the green line below).

Just like in the case of GST2, CHI can be deployed in any smart contract in a relatively simple manner using Deployer.eth meaning other aggregators can integrate CHI token to save fees for their own end users, including the 0x API. For now though, the majority of CHI adoption is through 1inch where the token is held in more than 1.6k addresses.

So how has CHI been used since launching? As expected, we can see in the graph below that when gas prices started rising in the middle of July, CHI mint activity grounded to a halt while CHI freed steadily rose. This freeing of CHI by holders provides crucial context for how 1inch exchange volume was able to increase 94% in July despite the rising gas prices.

To date, 1inch users have been able to save a total of $300k through the use of both the GST2 and CHI token integrations with most savings occurring since the launch of CHI (June onwards). July experienced the highest savings of any month by far, with users saving a total of $154k. It is important to note here that the increase in savings for users from June onwards was likely the combination of improved CHI architectural design as well as increased adoption of the 1inch aggregator more generally.

Closing remarks

As liquidity in DeFi continues to grow and be fragmented, DEX aggregators can serve users with even better experiences through refined UIs and improved tooling. Within this niche, 1inch has emerged as the clear leader. With variation in liquidity aggregation results likely to become insignificant between DEX aggregators, 1inch will likely formalise a token economic model in order to encourage long-term protocol participation and ensure its market dominance is sustained.

An exciting but challenging area of future development work for DEX aggregators will revolve around interoperability - the ability to securely tap into liquidity sourced beyond Ethereum's ecosystem, such as Tezos or Cosmos. In this sense, the next biggest opportunity for these projects will come from recognising that liquidity is not only fragmented at the DEX layer but also for base layer protocols themselves.